By capSpire’s Advisory Team

The Renewable Identification Number (RIN) market has become a critical component of U.S. energy and environmental policy, yet it remains one of the least understood areas of compliance trading. Designed under the Renewable Fuel Standard (RFS), RINs serve as tradable credits that track and verify the blending of renewable fuels into the nation’s fuel supply. For energy and commodity trading organizations, understanding how the RINs market works is no longer optional, it directly impacts compliance costs, trading strategies, and risk management practices.

At capSpire, we help clients navigate this evolving landscape by aligning their trading and risk systems with the complexities of RINs management, ensuring they remain both compliant and competitive.

Background to the Renewable Fuel Standard Program (RFS)

The RFS program was created by the Environmental Protection Agency (EPA) under the Energy Policy Act of 2005 and expanded by the Energy Independence and Security Act of 2007. Its purpose was to compel the energy industry to blend renewable fuels into gasoline and reduce the quantity of fossil fuels utilized. The original standard only included gasoline products. In 2010 the RFS rule was expanded to cover gasoline and diesel intended for highway use. The RFS2 program identifies categories of renewable fuels and creates target volumes for each of the categories based on their elimination of greenhouse gas emissions. The program introduced the use of identification numbers administered by the EPA to ensure compliance with the standard. These Renewable Identification Numbers (RINs) are generated for each gallon of renewable fuel produced.

What Are Renewable Identification Numbers (RINs)?

RINs serve as compliance credits for Obligated parties that must satisfy their Renewable Volume Obligations (RVO).

RIN Generation

Renewable fuel producers generate a RIN for every gallon of renewable fuel produced. Each RIN captures key information, such as Production facility, production year, batch number, and the renewable fuel classification. The RIN is entered into the EPA Moderated Transaction System (EMTS) for reporting and compliance.

RIN Classification

RINs are classified into distinct categories based on the type of renewable fuel and its GHG reduction potential. Each category satisfies different RVO compliance requirements:

- D6 RINs: Conventional biofuels like corn-based ethanol.

- D5 RINs: Advanced biofuels, such as renewable diesel from non-food oils and renewable jet fuel.

- D4 RINs: Biomass-based diesel, including biodiesel and renewable diesel.

- D3 RINs: Cellulosic biofuels, including renewable natural gas (RNG) from landfill gas and cellulosic ethanol.

Biofuels Beyond Ethanol and Biodiesel

While ethanol and biodiesel are the most well-known renewable fuels, several other biofuels also generate RINs:

- Renewable Diesel (D4 RINs): Chemically identical to petroleum diesel and usable without blending limits.

- Cellulosic Biofuel (D3 RINs): Made from non-food feedstocks like corn stover, wood chips, and municipal solid waste.

- Renewable Natural Gas (RNG) (D3 or D5 RINs): Produced from methane captured at landfills, wastewater treatment plants, and livestock operations.

- Renewable Jet Fuel (D5 RINs): Used in aviation as a sustainable alternative to fossil-based jet fuel.

- Renewable Heating Oil (D4 or D5 RINs): A renewable substitute for traditional heating oil.

How are fuels qualified for the RFS program?

Companies that produce renewable fuels need to apply for fuel pathways, a process that qualifies the fuel for the RFS program’s RIN type identification. The primary objective of the fuel pathways is to analyze the lifecycle greenhouse gas (GHG) emission percent reduction relative to the conventional fuel being displaced. The GHG reduction percentage of the renewable fuel will then determine the RIN type tagged to that fuel (“D” code) when it is introduced to the market.

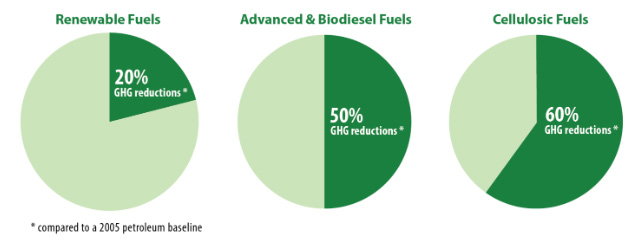

The renewable fuel types in the RFS program are depicted in the graphic below. D6 RINs are represented in the “Renewable Fuels” category. D4 and D5 RINs are included in “Advanced & Biodiesel Fuels”. D3 RINs are accounted for in “Cellulosic Fuels”. The metric accounts for direct and indirect emission changes.

GHG Displacement by RIN Type

Source: EPA

Nationwide Renewable Fuel Consumption Targets

The EPA sets annual renewable fuel consumption targets under the RFS program. These targets are expressed both as a total required volume of renewable fuels and as a percentage of total motor fuel consumed in the United States. The goal is to gradually increase the use of renewable fuels to reduce greenhouse gas (GHG) emissions, enhance energy security, and support the growth of the renewable fuel industry.

Types of Renewable Fuel Targets

The EPA’s volume requirements are divided into four main categories, each with a specific GHG reduction threshold:

- Total Renewable Fuel (e.g., corn ethanol, biodiesel, renewable diesel, RNG)

- Minimum GHG reduction: 20% (relative to petroleum-based fuels)

- Advanced Biofuel (e.g., biodiesel, renewable diesel, cellulosic biofuel)

- Minimum GHG reduction: 50%

- Biomass-Based Diesel (e.g., biodiesel, renewable diesel)

- Minimum GHG reduction: 50%, but it must also meet unique diesel fuel criteria.

- Cellulosic Biofuel (e.g., RNG from landfill gas, cellulosic ethanol)

- Minimum GHG reduction: 60%

Each category has a specific annual volume target set by the EPA, with cellulosic biofuel typically having the most ambitious GHG reduction target and the lowest production volume due to its technological complexity.

How the Targets Are Set and Adjusted

Each year, the EPA proposes and finalizes volume requirements for these categories based on factors such as:

- Projected fuel consumption: Adjusting targets as gasoline and diesel demand fluctuates.

- Production capacity and market conditions: Balancing ambitious goals with realistic production capacity.

- GHG reduction targets and long-term goals: Ensuring the targets align with U.S. climate commitments.

The EPA’s Annual RFS Rulemaking process is critical for ensuring these targets remain achievable while promoting the growth of advanced and cellulosic biofuels. In addition to setting volumes, the EPA considers public comments and market feedback to adjust targets as needed.

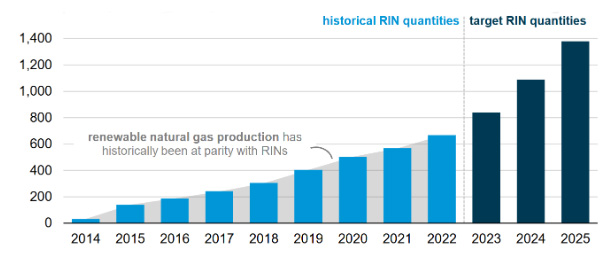

Biofuel Production & New RFS Volume Targets (Million Gal.)

Source: EPA

According to the EPA, the goal is to continue to increase total renewable fuel production in the U.S., a step toward reducing reliance on conventional fuels and promoting sustainable energy alternatives. Projections and target quantities are not available yet for 2026 as of the writing of this memo.

Renewable Volume Obligations (RVO)

The RVO represents the annual renewable fuel blending requirement for obligated parties. An obligated party is a refiner or importer of gasoline and distillate. They are the ultimate consumer of the RIN credit and responsible for the reporting and retiring of the RIN. The obligated party will calculate and certify their RVO for reporting to the EPA. The RVO is calculated by applying the RFS volume percentage to the total amount of non-renewable gasoline or distillate (NRGV) sold by the fuel producer or supplier.

How RINs Ensure Compliance of RFS

Transfer and reclassification of RINs

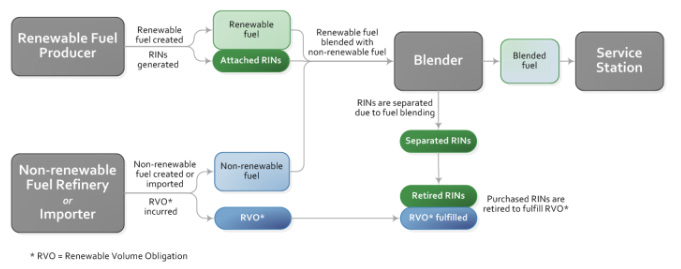

Producers of renewable fuels will generate and log the RIN in EMTS when a batch is created. Upon creation the RIN is classified as ‘attached’ and given the designation of K1. When the renewable fuel is sold, the RIN will ‘transfer’ to the buyer of the renewable fuel. As the renewable fuel is blended with gasoline or distillate the RIN is ‘separated’ and reclassified as K2. Every transfer of RINs that occur is logged and tracked in EMTS.

Obligated vs. Non-Obligated Parties

Every counterparty that transacts RINs has a reporting obligation with the EPA, however obligated parties are responsible for ensuring the RVO requirement has been met and ultimately ‘retires’ the RIN. This disconnect in the supply chain has created a RIN market. The table below illustrates the RIN lifecycle.

As you can see the Obligated party produces gasoline and distillate that will eventually be blended with renewable fuel, however if they do not participate in the downstream market, they will have to buy RINs to fulfill their RVO obligation. In contrast the non-obligated party ‘the blender’ will receive RINs and will need to sell these RINs to the obligated parties.

RIN Lifecycle

Source: EPA

The Evolution of the RIN Market

Refiners and retailers with blending capabilities often generate surplus RINs by blending renewable fuels beyond the levels required for compliance. The excess RINs can be carried over (up to 20%, per EPA regulations) or sold as paper credits in the market.

RINs are actively bought and sold on the market, with price determined by factors such as vintage year and RIN type. Key points include:

- The trading of RINs and passing down of RIN value is not necessarily the same. Sometimes RIN values are passed along without the underlying asset itself (i.e., the RIN).

- In Q4, the EPA permits trading of next year’s RIN credits.

- Future credits cannot satisfy current-year obligations but can be reserved for upcoming mandates.

- Market dynamics, such as blending volumes, renewable fuel prices, and speculative trading, contribute to price changes and at times can cause RIN prices to be volatile.

While the EPA designed RIN costs to be passed to end consumers, changes in RIN prices have not directly translated to gas pump prices. Numerous factors influence retail pricing, creating exposure to RIN price volatility for companies unable to meet their RVOs through blending.

Blending Economics and RIN Profitability

Access to renewable fuels significantly impacts a company’s ability to blend cost-effectively. For example, ethanol-rich regions like the Midwest provide an advantage for companies scaling renewable fuel blending.

Key benefits of additional blending:

- Cost Savings: Ethanol often trades at a discount to gasoline, lowering production costs.

- Competitive Pricing: Slightly increasing ethanol content (e.g., moving from E10 to E15) can reduce fuel prices, offering a competitive edge.

- Vehicle Compatibility: According to the Renewable Fuels Association (RFA), over 80% of vehicles can transition from E10 to E15 without equipment modifications, creating a large market for E15 adoption.

Blenders who seize this opportunity have generated significant profits by exceeding blending requirements, resulting in excess RIN credits. A simple RIN profit and loss calculator can illustrate how switching from E10 to E15 can boost profitability, even for a gas station selling a million gallons of fuel annually.

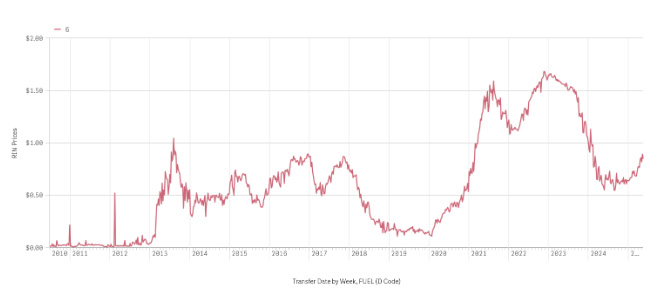

RIN Market Volatility

Since the establishment of the RFS program in 2010 there has been heightened volatility in the RINs market. Several factors have contributed to the Volatility:

- Regulatory uncertainty

- The EPA’s setting of RVO is often delayed and has been revised

- Changing political administrations shift priorities

- Small refinery exemptions (SREs)

- The EPA has granted SRE’s in large numbers causing a reduction in the demand for RINs causing prices to fall.

- When SREs are tightened or denied, RIN demand spikes, increasing prices sharply

- Legal and Court Rulings

- Court decisions on EPA authority or blending mandates

- Market Speculation and Trading Liquidity

- RINs is a thinly traded market, small shifts in speculative positions can create exaggerated price moves

- Illiquid Markets

- D3 generation comes from a small group of producers whose volumes are constrained by technological and feedstock challenges

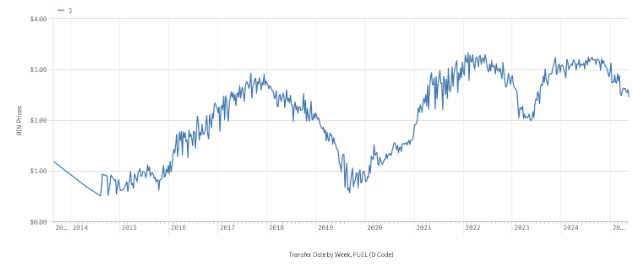

D6 Rin Prices by transfer Week

Source EPA

D3 Rin Prices by transfer Week

Source EPA

Current RIN Landscape and Criticism

Despite its success, the RIN program has faced several challenges:

- Disparities in Refining Access

Fully integrated refineries and retailers with blending facilities benefit more from the program, while smaller refiners without blending capabilities bear higher RIN costs, impacting their profit margins. - Fraudulent RINs

Cases of false paper RINs have raised concerns about program transparency. The EPA has increased audits to ensure compliance and prevent fraud. - Technological Advancements and Resistance

With the EPA raising volume targets for advanced fuels like cellulosic ethanol (D3), industry readiness to meet these goals remains uncertain. The term “E10 blend wall” highlights industry concerns about significant infrastructure and equipment changes required to accommodate higher ethanol blends like E15 or E25.

The Road Ahead

The RFS program plays a pivotal role in advancing renewable fuels and reducing greenhouse gas emissions. While challenges remain, technological progress and strategic incentives offer opportunities for growth. The transition to higher renewable fuel blends will require cooperation across the energy and automotive sectors, but the potential benefits for the environment and energy independence make it a goal worth pursuing.

How capSpire can help

At capSpire, we’ve helped clients go beyond basic RINs compliance to achieve real business value. From integrating CTRM systems with EMTS for real-time RINs tracking, to configuring workflows that streamline reporting, to building advanced risk models that provide deeper P&L insight, we help to ensure trading organizations stay ahead of market and regulatory demands. With forecasting and position tracking built directly into CTRM, our clients gain the transparency, control, and confidence they need to manage RINs exposure effectively and turn it into a strategic advantage.

What sets capSpire apart is not only our ability to drive strategic and operational excellence but also our recognized expertise in Renewable Identification Numbers (RINs). We understand the complexities of navigating RIN markets, providing businesses with the tools, insights, and strategies needed to manage compliance and capitalize on opportunities.

Let’s talk.